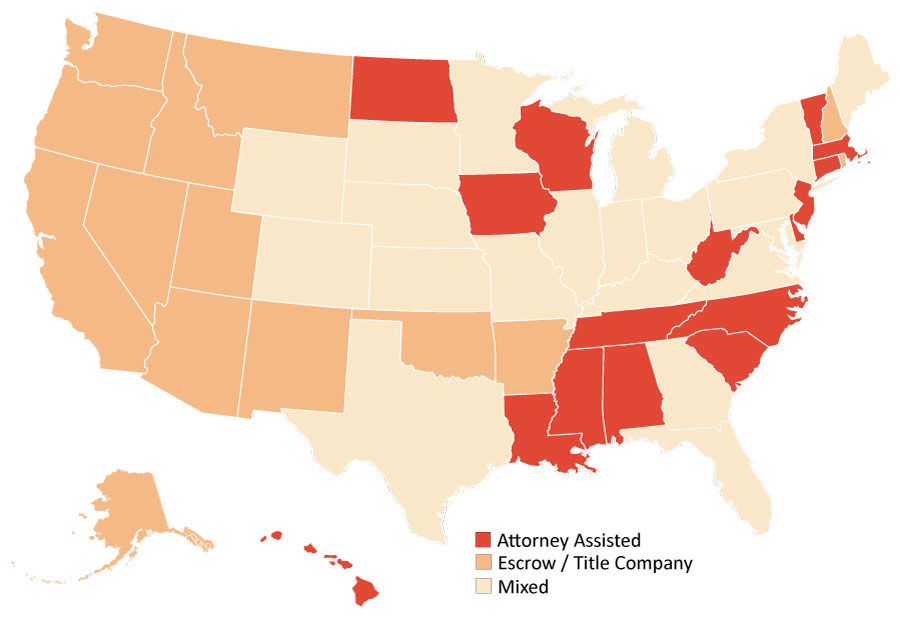

State by State Closing Guide

This summary is merely a general reference guide. Local practices within your city or county may differ. Contact a local title company or real estate attorney for specific information.

This is not intended as a legal advice, but merely as a general reference guide.” For further explanation and an in-depth resource guide for your state refer to The Complete Guide to Your Real Estate Closing, available at www.amazon.com or sandygadow.com/learn.

Please choose a state:

[ Alabama ] [ Alaska ] [ Arizona ] [ Arkansas ] [ California ] [ Colorado ] [ Connecticut ] [ Deleware ] [ District of Columbia ] [ Florida ] [ Georgia ] [ Hawaii ] [ Illinois ] [ Idaho ] [ Indiana ] [ Iowa ] [ Kansas ] [ Kentucky ] [ Louisiana ] [ Maine ] [ Maryland ] [ Massachusetts ] [ Michigan ] [ Minnesota ] [ Mississippi ] [ Missouri ] [ Montana ] [ Nebrasca ] [ Nevada ] [ New Hampshire ] [ New Jersey ] [ New Mexico ] [ New York ] [ North Carolina ] [ North Dakota ] [ Ohio ] [ Oklahoma ] [ Oregon ] [ Pennsylvania ] [ Rhode Island ] [ South Carolina ] [ South Dakota ] [ Tennessee ] [ Texas ] [ Utah ] [ Vermont ] [ Virginia ] [ Washington ] [ West Virginia ] [ Wisconsin ] [ Wyoming ]

Attorneys and title companies handle closings. Conveyance is by warranty deed. Mortgages are the customary security instruments. Foreclosures are non-judicial. Foreclosure notices are published once a week for three weeks on a county-by-county basis. The foreclosure process takes a minimum of 21 days from the date of first publication. After the sale, there is a one-year redemption period. Alabamans use ALTA policies to insure titles. Buyers and sellers negotiate who is going to pay the closing costs and usually split them equally. Property taxes are due and payable annually on October 1st.

Title companies, lenders, and private escrow companies all handle real estate escrows. Conveyance is by warranty deed. Deeds of trust with private power of sale are the customary security instruments. Foreclosures take 90-120 days. Alaskans use ALTA owner’s and lender’s policies with standard endorsements. There are no documentary or transfer taxes. Buyer and seller usually split the closing costs. Property tax payment dates vary throughout the state.

Title companies and title agents both handle closings. Conveyance is by warranty deed. Whereas deeds of trust are the security instruments most often used, mortgages and “agreements for sale” are used approximately 20% of the time. Foreclosure depends upon the security instrument. For deeds of trust, the foreclosure process takes about 91 days. Arizonans use ALTA owner’s and lender’s policies, standard or extended, with standard endorsements. The seller customarily pays for the owner’s policy, and the buyer pays for the lender’s policy. They split escrow costs otherwise. There are no documentary, transfer, or mortgage taxes. The first property tax installment is due October 1st and delinquent November 1st; the second half is due March 1st and delinquent May 1st. Arizona is a community-property state.

Title agents handle escrows, and attorneys conduct closings. Conveyance is by warranty deed. Mortgages are the customary security instruments. Foreclosure requires judicial proceedings, but there are no minimum time limits for completion. Arkansans use ALTA policies and endorsements and receive a 40% discount for reissuance of prior policies. Buyers and sellers pay their own escrow costs. The buyer pays for the lender’s policy; the seller pays for the owner’s. The buyer and seller split the state documentary tax. Property taxes come due three times a year as follows: the third Monday in April, the third Monday in July, and the tenth day of October.

CALIFORNIA

Not only do escrow procedures differ between Northern and Southern California, they also vary somewhat from county to county. Title companies handle closings through escrow in Northern California, whereas escrow companies and lenders handle them in Southern California. Conveyance is by grant deed. Deeds of trust with private power of sale are the security instruments used throughout the state. Foreclosure requires a three-month waiting period after the recording of the notice of default. After the waiting period, the notice of sale is published each week for three consecutive weeks. The borrower may reinstate the loan at any time prior to five business days before the foreclosure sale. All in all, the procedure takes about four months. Californians have both ALTA and CLTA policies available. In Southern California, sellers pay the title insurance premium and the transfer tax. Buyer and seller split the escrow costs. In the Northern California counties of Amador, Merced, Plumas, San Joaquin, and Siskiyou, buyers and sellers share title insurance and escrow costs equally. In Butte County, sellers pay 75%; buyers pay 25%. In Alameda, Calaveras, Colusa, Contra Costa, Lake, Marin, Mendocino, San Francisco, San Mateo, Solano, and Sonoma counties, buyers pay for the title insurance policy, whereas sellers pay in the other Northern California counties. Each California county has its own transfer tax; some cities have additional charges. Property taxes may be paid annually on or before December 10th, or semiannually by December 10th and April 10th. Annual taxes are set at no more than 1 percent of the property’s base value or purchase price. Each year following this, a two percent increase is permissible. (Proposition 13). A property transfer between husband and wife will not result in a new tax assessment of one percent of the fair market value.The homeowner’s exemption allows an owner to be exempt of the first $7,000 of the property’s full cash value. This exemption is allowed only for primary residences. Homeowner must obtain a form from the county tax assessor, and submit it by February 15 of the current tax year to be eligible for the exemption. Californians over the age of 55 also have the option of moving primary residences and taking their prior “old” tax base with them to the new property. This exception may be used only once in a lifetime. Referred to as the” Senior Citizen’s Replacement Dwelling Benefit”, Proposition 60 was a constitutional amendment approved by the voters in 1986. It is codified in Section 69.5 of the Revenue & Taxation Code, and allows the transfer of an existing Proposition 13 base year value from a former residence to a replacement residence, if certain conditions are met. California is a community-property state.

The homeowner’s exemption allows an owner to be exempt of the first $7,000 of the property’s full cash value. This exemption is allowed only for primary residences. Homeowner must obtain a form from the county tax assessor, and submit it by February 15 of the current tax year to be eligible for the exemption. Californians over the age of 55 also have the option of moving primary residences and taking their prior “old” tax base with them to the new property. This exception may be used only once in a lifetime. Referred to as the” Senior Citizen’s Replacement Dwelling Benefit”, Proposition 60 was a constitutional amendment approved by the voters in 1986. It is codified in Section 69.5 of the Revenue & Taxation Code, and allows the transfer of an existing Proposition 13 base year value from a former residence to a replacement residence, if certain conditions are met. California is a community-property state.

COLORADO

Title companies, brokers, and attorneys all may handle closings. Conveyance is by warranty deed. Deeds of trust are the customary security instruments. Public trustees must sell foreclosure properties within 45-60 days after the filing of a notice of election and demand for sale, but they will grant extensions up to six months following the date of the originally scheduled sale. Subdivided properties may be redeemed within 75 days after sale; agricultural properties may be redeemed within 6 months after sale. The first junior lien holder has 10 additional days to redeem, and the second and other junior lienholders have an additional 5 days each. The public trustee is normally the trustee shown on the deed of trust, a practice unique to Colorado. Foreclosures may be handled judicially. Coloradans have these title insurance policy options: ALTA owner’s, lender’s, leasehold, and construction loan; endorsements are used, too. Although they are negotiable, closing costs are generally split between buyer and seller, and seller normally pays for title insurance. Sellers pay the title insurance premium and the documentary transfer tax. Property taxes may be paid annually at the end of April or semiannually at the ends of February and July.

Attorneys normally conduct closings. Most often conveyance is by warranty deed, but quitclaim deeds do appear. Mortgages are the security instruments. Judicial foreclosures are the rule, either by a suit in equity for strict foreclosure or by a court decree of sale. Court decreed sales preclude redemption, but strict foreclosures allow redemption for 3-6 months, depending upon the discretion of the court. There are lender’s and owner’s title insurance policies available with various endorsements. Buyers customarily pay for examination and title insurance, while sellers pay the documentary and conveyance taxes. Property tax payment dates vary by town.DELAWARE

Attorneys handle closings. Although quitclaim and general warranty deeds are sometimes used, most conveyances are by special warranty deeds. Mortgages are the security instruments. Foreclosures are judicial and require 90-120 days to complete. ALTA policies and endorsements are prevalent. Buyers pay closing costs and the owner’s title insurance premiums. Buyers and sellers share the state transfer tax. Property taxes are on an annual basis and vary by county.

Attorneys handle closings. Although quitclaim and general warranty deeds are sometimes used, most conveyances are by special warranty deeds. Mortgages are the security instruments. Foreclosures are judicial and require 90-120 days to complete. ALTA policies and endorsements are prevalent. Buyers pay closing costs and the owner’s title insurance premiums. Buyers and sellers share the state transfer tax. Property taxes are on an annual basis and vary by county.

Attorneys, title insurance companies, or their agents may conduct closings. Conveyances are by bargain-and-sale deeds. Though mortgages are available, the deed of trust, containing private power of sale, is the security instrument of choice. Foreclosures require at least six weeks and start with a 30-day notice of sale sent by certified mail. ALTA policies and endorsements insure title. Buyers generally pay closing costs, title insurance premiums, and recording taxes. Sellers pay the transfer tax. Property taxes fall due annually or if they’re less than $100,000, semiannually, on September 15th and March 31st.

Title companies and attorneys handle closings. Conveyance is by warranty deed. Mortgages are the customary security instruments. Foreclosures are judicial and take about 3 months. They involve service by the sheriff, a judgment of foreclosure and sale, advertising, public sale, and finally issuance of a certificate of sale and certificate of title. ALTA policies are commonplace. Buyers pay the escrow and closing costs, while county custom determines who pays for the title insurance. Sellers pay the documentary tax. Property taxes are payable annually, but the due and delinquent dates are months apart, November 1st and April 1st. Interestingly, in Palm Beach County the legislature has decided to lower the tax rate for home owners in 2023-2024 due to a surplus of funds collected due to the increase in valuation of residential properties

Under Florida law, a widow or widower has the right to live in their deceased spouse’s house for the remainder of his or her life, even if the home is willed to someone else. A Homestead Exemption exists for an owner’s residence in Florida. Florida’s exemption is unique because it lacks any monetary cap on the homestead protection, while other states which offer a homestead exemption usually place a limit on the valuation which can be protected.

Attorneys generally take care of closings. Conveyance is by warranty deed. Security deeds are the security instruments. Foreclosures are non-judicial and take little more than a month because there’s a power of attorney right in the security deed. Foreclosure advertising must appear for 4 consecutive weeks prior to the first Tuesday of the month; that’s when foreclosure sales take place. Georgians use ALTA title insurance policies, including owner’s and lender’s, and they use binders and endorsements. Buyers pay title insurance premiums and also closing costs usually. Sellers pay transfer taxes. Property tax payment dates vary across the state.HAWAII

By law, only attorneys may prepare property transfer documents, but there are title and escrow companies available to handle escrows and escrow instructions. Conveyance of fee-simple property is by warranty deed; conveyance of leasehold property, which is common throughout the state, is by assignment of lease. Condominiums are everywhere in Hawaii and may be fee simple or leasehold. Sales of some properties, whether fee simple or leasehold, are by agreement of sale. Mortgages are the security instruments. Hawaiians use judicial foreclosures rather than powers of sale for both mortgages and agreements of sale. These foreclosures take 6-12 months and sometimes more, depending upon court schedules. Title companies issue ALTA owner’s and lender’s policies and make numerous endorsements available. Buyers and sellers split escrow fees. Sellers pay the title search costs and the conveyance tax. Buyers pay title insurance premiums for the owner’s and lender’s policies. Property taxes come due twice a year, on February 20th and again on August 20th.

By law, only attorneys may prepare property transfer documents, but there are title and escrow companies available to handle escrows and escrow instructions. Conveyance of fee-simple property is by warranty deed; conveyance of leasehold property, which is common throughout the state, is by assignment of lease. Condominiums are everywhere in Hawaii and may be fee simple or leasehold. Sales of some properties, whether fee simple or leasehold, are by agreement of sale. Mortgages are the security instruments. Hawaiians use judicial foreclosures rather than powers of sale for both mortgages and agreements of sale. These foreclosures take 6-12 months and sometimes more, depending upon court schedules. Title companies issue ALTA owner’s and lender’s policies and make numerous endorsements available. Buyers and sellers split escrow fees. Sellers pay the title search costs and the conveyance tax. Buyers pay title insurance premiums for the owner’s and lender’s policies. Property taxes come due twice a year, on February 20th and again on August 20th.

Closings are handled through escrow. Conveyance is by warranty deed or corporate deed, though often there are contracts of sale involved. Either mortgages or deeds of trust may be the security instruments. Deeds of trust which include power of sale provisions are restricted to properties in incorporated areas and properties elsewhere which don’t exceed 20 acres. After the notice of default has been recorded, deed-of-trust foreclosures take at least 120 days, and there’s no redemption period. Judicial foreclosures for mortgages take about a year, depending upon court availability, and there’s a 6-12 month redemption period after that, depending on the type of property involved. Idahoans use ALTA policies and various endorsements. Buyers and sellers split escrow costs in general and negotiate who’s going to pay the title insurance premiums. There are no documentary taxes, mortgage taxes, or transfer taxes, but there are property taxes, and they’re due annually in November and delinquent on December 20th or semiannually on December 20th and June 20th. Idaho is a community-property state.

Title companies, lenders, and attorneys may conduct closings, but only attorneys may prepare documents. Lenders generally hire attorneys and have them prepare all the paperwork. Conveyance is by warranty deed. Recorded deeds must include a declaration of the sales price. Mortgages are the customary security instruments. Judicial foreclosure is mandatory and takes at least a year from the filing of the default notice to the expiration of the redemption period. Illinoisans use ALTA policies. Buyers usually pay the closing costs and the lender’s title insurance premiums; sellers pay the owner’s title insurance premiums and the state and county transfer taxes. Property tax payment dates vary. Larger counties typically schedule them for March 1st and September 1st, and smaller counties schedule them for June 1st and September 1st.

Title companies, lenders, real estate agents, and attorneys handle closings. Conveyance is by warranty deed. Mortgages are the customary security instruments. Judicial foreclosures are required; execution of judgments varies from 3 months after filing of the complaint in cases involving mortgages drawn up since July 1, 1975, to 6 months for those drawn up between January 1, 1958, and July 1, 1975, to 12 months for those drawn up before that. Immediately following the execution sale, the highest bidder receives a sheriff’s deed. Hoosiers use ALTA policies and certain endorsements. Buyers usually pay closing costs and the lender’s title insurance costs, while sellers pay for the owner’s policy. There are no documentary, mortgage, or transfer taxes. Property taxes fall due on May 10th and November 10th.

Attorneys may conduct closings, and so may real estate agents. Conveyance is usually by warranty deed. Mortgages and deeds of trust are both authorized security instruments, but lenders prefer mortgages because deeds of trust do not circumvent judicial foreclosure proceedings anyway. Those proceedings take at least 4 -6 months. Since Iowa is the only state which does not authorize private title title insurance, Iowans who want it must go through a state administered title company or fund. Buyers and sellers share the closing costs; sellers pay the documentary taxes. Property taxes are due July 1st based upon the previous January’s assessment.

KANSAS

Title companies, lenders, real estate agents, attorneys, and independent escrow firms all conduct closings. Anyone who conducts a title search must be a licensed abstracter, a designation one receives after passing strict tests and meeting various requirements. Because many land titles stem from Indian origins, deeds involving Indians as parties to a transaction go before the Indian Commission for approval. Conveyance is by warranty deed. Mortgages are the customary security instruments. Judicial foreclosures, the only ones allowed, take about 6 months from filing to sale. Redemption periods vary, the longest being 12 months. Kansans use ALTA policies and endorsements. Buyers and sellers divide closing costs. Buyers pay the lender’s policy costs and the state mortgage taxes; sellers pay for the owner’s policy. Property taxes come due November 1st, but they needn’t be paid in a lump sum until December 31st. They may also be paid in two installments, the first on December 20th and the second on June 20th.

KENTUCKY

Attorneys conduct closings. Conveyance is by grant deed or by bargain-and-sale deed. Deeds must show the name of the preparer, the amount of the total transaction, and the recording reference by which the grantor obtained title. Mortgages are the principal security instruments because deeds of trust offer no power-of-sale advantages. Enforcement of any security instrument requires a decree in equity, a judicial foreclosure proceeding. Kentuckians use ALTA policies and endorsements. Sellers pay closing costs; buyers pay recording fees. Responsibility for payment of title insurance premiums varies according to locale. Property taxes are payable on an annual basis; due dates vary from county to county.

LOUISIANA

Either attorneys or corporate title agents may conduct closings, but a notary must authenticate the documentation. Conveyance is by warranty deed or by act of sale. Mortgages are the security instruments generally used in commercial transactions, while vendor’s liens and seller’s privileges are used in other purchase money situations. Foreclosures are swift (60 days) and sure (no right of redemption). Successful foreclosure sale bidders receive an adjudication from the sheriff. Louisianians use ALTA owner’s and lender’s policies and endorsements. Buyers generally pay the title insurance and closing costs. There are no mortgage or transfer taxes. Property tax payment dates vary from parish to parish (parishes are like counties). Louisiana is a community-property state.

MAINE

Attorneys conduct closings. Conveyance is by warranty or quitclaim deed. Mortgages are the security instruments. Foreclosures may be initiated by any of the following: an act of law for possession; entering into possession and holding the premises by written consent of the mortgagor; entering peaceably, openly, and unopposed in the presence of two witnesses and taking possession; giving public notice in a newspaper for three successive weeks and recording copies of the notice in the Registry of Deeds, and then recording the mortgage within 30 days of the last publication; or by a bill in equity (special cases). In every case, the creditor must record a notice of foreclosure within 30 days. Judicial foreclosure proceedings are also available. Redemption periods vary from 90-365 days depending on the method of foreclosure. Mainers use ALTA owner’s and lender’s policies and endorsements. Buyers pay closing costs and title insurance fees; buyers and sellers share the documentary transfer taxes. Property taxes are due annually on April 1st.

Attorneys conduct closings, and there has to be a local attorney involved. Conveyance is by grant deed, and the deed must state the consideration involved. Although mortgages are common in some areas, deeds of trust are more prevalent as security instruments. Security instruments may include a private power of sale, so it naturally is the foreclosure method of choice. Marylanders use ALTA policies and endorsements. Buyers pay closing costs, title insurance premiums, and transfer taxes. Property taxes are due annually on July 1st. Police officers in Prince George’s County who are first-time home buyers get a break on their transfer taxes at closing under a law that took effect July 1, 2006. Officers pay 1 percent of the purchase price rather than 14%, the regular rate. County school teachers were made eligible for the same tax break in an earlier law without the first-time buyer limitation. Teachers must commit to living in the house for at least three years and maintain their teaching position with the county during that time.

Attorneys handle closings. Conveyance is by warranty deed in the western part of the state and by quitclaim deed in the eastern part. Mortgages with private power of sale are the customary security instruments. Creditors forced to foreclose generally take advantage of the private power of sale, but they may foreclose through peaceable entry (entering unopposed in the presence of two witnesses and taking possession for 3 years) or through the rarely used judicial writ of entry. Frequently, cautious creditors will foreclose through both power of sale and peaceable entry. People in Massachusetts use ALTA owner’s and lender’s title insurance policies and endorsements. Buyers pay closing costs and title insurance fees, except in Worcester, where sellers pay. Sellers pay the documentary taxes. Property taxes are payable in two installments, November 1st and May 1st.

Title companies, lenders, real estate agents, and attorneys may conduct closings. Conveyance is by warranty deed which must give the full consideration involved or be accompanied by an affidavit which does. Many transactions involve land contracts. Mortgages are the security instruments. Private foreclosure is permitted; it requires advertising for 4 consecutive weeks and a sale at least 28 days following the date of first publication. The redemption period ranges from 1 to 12 months. Michiganders use ALTA policies and endorsements. Buyers generally pay closing costs and the lender’s title insurance premium, and sellers pay the state transfer tax and the owner’s title insurance premium. Those property taxes which pay for city and school expenses fall due July 1st; others (county taxes, township taxes, and some school taxes) fall due on the first of December. In many tax jurisdictions, taxpayers may opt to pay their taxes in two equal installments without penalty.MINNESOTA

Title companies, lenders, real estate agents, and attorneys may conduct closings. Conveyance is by warranty deed. Although deeds of trust are authorized, mortgages are the customary security instruments. The redemption period following a foreclosure is 6 months in most cases; it is 12 months if the property is larger than 10 acres or the amount claimed to be due is less than 2/3 of the original debt. This is a strong abstract state. Typically a buyer will accept an abstract and an attorney’s opinion as evidence of title, even though the lender may require title insurance. People in the Minneapolis-St. Paul area use the Torrens system. Minnesotans use ALTA policies. Buyers pay the lender’s and owner’s title insurance premiums and the mortgage tax. Sellers usually pay the closing fees and the transfer taxes. Property taxes are due on May 15th and October 15th.

Title companies, lenders, real estate agents, and attorneys may conduct closings. Conveyance is by warranty deed. Although deeds of trust are authorized, mortgages are the customary security instruments. The redemption period following a foreclosure is 6 months in most cases; it is 12 months if the property is larger than 10 acres or the amount claimed to be due is less than 2/3 of the original debt. This is a strong abstract state. Typically a buyer will accept an abstract and an attorney’s opinion as evidence of title, even though the lender may require title insurance. People in the Minneapolis-St. Paul area use the Torrens system. Minnesotans use ALTA policies. Buyers pay the lender’s and owner’s title insurance premiums and the mortgage tax. Sellers usually pay the closing fees and the transfer taxes. Property taxes are due on May 15th and October 15th.

Attorneys conduct real estate closings. Conveyance is by warranty deed. Deeds of trust are the customary security instruments. Foreclosure involves a non-judicial process which takes 21-45 days. Mississippians use ALTA policies and endorsements. Buyers and sellers negotiate the payment of title insurance premiums and closing costs. There are no documentary, mortgage, or transfer taxes. Property taxes are payable on an annual basis and become delinquent February 1st.

Title companies, lenders, real estate agents, and attorneys may conduct closings. In the St. Louis area, title company closings predominate. In the Kansas City area, an escrow company or a title company generally conducts the closing. Conveyance is by warranty deed. Deeds of trust are the customary security instruments and allow private power of sale. The trustee must be named in the deed of trust and must be a Missouri resident. Foreclosure involves publication of a sale notice for 21 days, during which time the debtor may redeem the property or file a notice of redemption. The foreclosure sale buyer receives a trustee’s deed. Missourians use ALTA policies and endorsements. Buyers and sellers generally split the closing costs. Sellers in western Missouri usually pay for the title insurance polices, while elsewhere the buyers pay. There are no documentary, mortgage, or transfer taxes. Property taxes are payable annually and become delinquent January 1st for the previous year.

Real estate closings are handled through escrow. Conveyance is by warranty deed, corporate deed, or grant deed. Mortgages, deeds of trust, and unrecorded contracts of sale are the security instruments. Mortgages require judicial foreclosure, and there’s a 6-12-month redemption period following sale. Foreclosure on deeds of trust involves filing a notice of default and then holding a trustee sale 120 days later. Montanans use ALTA policies and endorsements. Buyers and sellers split the escrow and closing costs; sellers usually pay for the title insurance policies. There are no documentary, mortgage, or transfer taxes. Montanans may pay their property taxes annually by November 30th or semi-annually by November 30th and May 31st.

NEBRASKA

Title companies, lenders, real estate agents, and attorneys all conduct closings. Conveyance is by warranty deed. Mortgages and deeds of trust are the security instruments. Mortgage foreclosures require judicial proceedings and take about 6 months from the date of the first notice when they’re uncontested. Deeds of trust do not require judicial proceedings and take about 90 days. Nebraskans use ALTA policies and endorsements. Buyers and sellers split escrow and closing costs; sellers pay the state’s documentary taxes. Property taxes fall due April 1st and August 1st.

NEVADA

Escrow similar to California’s is used for closings. Conveyance is by grant deed, bargain-and-sale deed, or quitclaim deed. Deeds of trust are the customary security instruments. Foreclosure involves recording a notice of default and mailing a copy within 10 days. Following the mailing there is a 35-day reinstatement period. After that, the beneficiary may accept partial payment or payment in full for a 3-month period. Then come advertising the property for sale for 3 consecutive weeks and finally the sale itself. All of this takes about 4 1/2 months. Nevadans use both ALTA and CLTA policies and endorsements. Buyers and sellers share escrow costs. Buyers pay the lender’s title insurance premiums; sellers pay the owner’s and the state’s transfer tax. Property taxes are payable in one, two, or four payments, the first one being due July 1st. Nevada is a community-property state.

Attorneys conduct real estate closings. Conveyance is by warranty or quitclaim deed. Mortgages are the customary security instruments. Lenders may foreclosure through judicial action or through whatever power of sale was written into the mortgage originally. Entry, either by legal action or by taking possession peaceably in the presence of two witnesses, is possible under certain legally stated conditions. There is a one-year right-of-redemption period. The people of New Hampshire use ALTA owner’s and lender’s policies. Buyers pay all closing costs and title fees except for the documentary tax; that’s shared with the sellers. Property tax payment dates vary across the state.

NEW JERSEY

Attorneys handle closings in northern New Jersey, and title agents customarily handle them elsewhere. Conveyance is by bargain-and-sale deed with covenants against grantors’ acts (equivalent to a special warranty deed). Mortgages are the most common security instruments though deeds of trust are authorized. Foreclosures require judicial action which take 6-9 months if they’re uncontested. New Jerseyites use ALTA owner’s and lender’s policies. Both buyer and seller pay the escrow and closing costs. The buyer pays the title insurance fees, and the seller pays the transfer tax. Property taxes are payable quarterly on the first of April, July, October, and January.

NEW MEXICO

Real estate closings are conducted through escrows. Conveyance is by warranty or quitclaim deed. Deeds of trust and mortgages are the security instruments. Foreclosures require judicial proceedings, and there’s a 9-month redemption period after judgment. New Mexicans use ALTA owner’s policies, lender’s policies, and construction and leasehold policies; they also use endorsements. Buyers and sellers share escrow costs equally; sellers pay the title insurance premiums. There are no documentary, mortgage, or transfer taxes. Property taxes are payable November 5th and April 5th. New Mexico is a community-property state.

NEW YORK

All parties to a transaction appear with their attorneys for closing. Conveyance is by bargain-and-sale deed. Mortgages are the security instruments in this lien-theory state. Foreclosures require judicial action and take several months if uncontested or longer if contested. New Yorkers use policies of the New York Board of Title Underwriters almost exclusively, though some use the New York State 1946 ALTA Loan Policy. Buyers generally pay most closing costs, including all title insurance fees and mortgage taxes. Sellers pay the state and city transfer taxes. Property tax payment dates vary across the state.

Attorneys or lenders may handle closings, and corporate agents issue title insurance. Conveyance is by warranty deed. Deeds of trust with private power of sale are the customary security instruments. Foreclosures are non-judicial, with a 10-day redemption period following the sale. The entire process takes between 45 and 60 days. North Carolinians use ALTA policies, but these require an attorneys opinion before they’re issued. Buyers and sellers negotiate the closing costs, except that buyers pay the recording costs, and sellers pay the document preparation and transfer tax costs. Property taxes fall due annually on the last day of the year.

NORTH DAKOTA

Lenders, together with attorneys, conduct closings. Conveyance is by warranty deed. Mortgages are the security instruments. Foreclosures require about 6 months, including the redemption period. North Dakotans base their title insurance on abstracts and attorneys’ opinions. Buyers usually pay for the closing, the attorney’s opinion, and the title insurance; sellers pay for the abstract. There are no documentary or transfer taxes. Property taxes are due March 15th and October 15th.

Title companies and lenders handle closings. Conveyance is by warranty deed. Dower rights require that all documents involving a married person must be executed by both spouses. Mortgages are the security instruments. Judicial foreclosures, the only kind allowed, require about 6-12 months. People in Ohio use ALTA policies; they get a commitment at closing and a policy following the recording of documents. Buyers and sellers negotiate who’s going to pay closing costs and title insurance premiums, but sellers pay the transfer taxes. Property tax payment dates vary throughout the state.

Title companies, lenders, real estate agents, and attorneys may conduct closings. Conveyance is by warranty deed. Mortgages are the usual security instruments. Foreclosures may be by judicial action or by power of sale if properly allowed for in the security instrument. Oklahomans use ALTA policies and endorsements. Buyers and sellers share the closing costs, except that the buyer pays the lender’s policy premium, the seller pays the documentary transfer tax, and the lender pays the mortgage tax. Property taxes may be paid annually on or before the last day of the year or semi-annually by December 31st and March 31st.

Closings are handled through escrow. Conveyance is by warranty or bargain-and-sale deed, but land sales contracts are common. Mortgage deeds and deeds of trust are the security instruments. Oregon attorneys usually act as trustees in non-judicial trust-deed foreclosures. Such foreclosures take 5 months from the date of the sale notice; defaults may be cured as late as 5 days prior to sale. Judicial foreclosures on either mortgages or trust deeds allow for a one-year redemption period following sale. Oregonians use ALTA and Oregon Land Title Association policies. Buyers and sellers split escrow costs and transfer taxes; the buyer pays for the lender’s title insurance policy, and the seller pays for the owner’s policy. Property taxes are payable the 15th of November, February, and May; if paid in full by November 15th, owners receive a 3% reduction.

Title companies, real estate agents, and approved attorneys may handle closings. Conveyance is by special or general warranty deed. Mortgages are the security instruments. Foreclosures take 1-6 months from filing through judgment plus another 2 months or more from judgment through sale. State law restricts aliens in owning real property with respect to acreage and income and includes special restrictions affecting farmland. Pennsylvanians use ALTA owner’s, lender’s, and leasehold policies. Buyers pay closing costs and title insurance fees; buyers and sellers split the transfer taxes. Property tax payment dates differ across the state.

RHODE ISLAND

Attorneys usually conduct closings, but banks and title companies may also conduct them. Conveyance is by warranty or quitclaim deed. Mortgages are the usual security instruments. Foreclosures follow the power-of-sale provisions contained in mortgage agreements and take about 45 days. Power-of-sale foreclosures offer no redemption provisions, whereas any other foreclosure method carries a 3-year right of redemption. Rhode Islanders use ALTA policies and endorsements. Buyers pay title insurance premiums and closing costs; sellers pay documentary taxes. Property taxes are payable annually, semi-annually, or quarterly with the first payment due in July.

Attorneys customarily handle closings. Conveyance is by warranty deed. Mortgages are most often the security instruments. Foreclosures are judicial and take 3-5 months depending on court schedules. Foreclosure sales take place on the first Monday of every month following publication of notice once a week for 3 consecutive weeks. South Carolinians use owner’s and lender’s ALTA policies and endorsements. Buyers pay closing costs, title insurance premiums, and state mortgage taxes; sellers pay the transfer taxes. Property tax payment dates vary across the state from September 15 to December 31.

SOUTH DAKOTA

Title companies, lenders, real estate agents, and attorneys may handle closings. Conveyance is by warranty deed. Mortgages are the usual security instruments. Foreclosures may occur through judicial proceedings or through the power-of-sale provisions contained in certain mortgage agreements. Sheriff’s sales follow publication of notice by 30 days. The redemption period allowed after sale of parcels smaller than 40 acres and encumbered by mortgages containing power of sale is 180 days; in all other cases, it’s a year. There’s a unique statute which stipulates that all land must be platted in lots or described by sectional references rather than by metes and bounds unless it involves property described in documents recorded prior to 1945.

There’s another unique statute called the Affidavit of Possession Statute. Certain exceptions aside, it provides that any person having an unbroken chain of title for 22 years thereafter has a marketable title free of any defects occurring prior to that 22-year period. South Dakotans use ALTA policies and endorsements. Sellers pay the transfer taxes and split the other closing costs, fees, and premiums with the buyers. Property taxes come due May 1st and November 1st.

A title company attorney, a party to the contract, a lender’s representative, or an outside attorney may conduct a closing. Conveyance is by warranty or quitclaim deed. Deeds of trust are the customary security instruments. Foreclosures, which are handled according to trustee sale provisions, are swift, that is, 22 days from the first publication of the notice until the public sale, and there is normally no right of redemption after that. Tennesseans use ALTA policies and endorsements. The payment of title insurance premiums, closing costs, mortgage taxes, and transfer taxes varies according to local practice. Property taxes are payable annually on the first Monday in October.

Title companies normally handle closings. Conveyance is by warranty deed. Deeds of trust are the most common security instruments. Following the posting of foreclosure sales at the local courthouse for at least 21 days, the sales themselves take place at the courthouse on the first Tuesday of the month. Texans use only Texas standard policy forms of title insurance. Buyers and sellers negotiate closing costs. There aren’t any documentary, transfer, or mortgage taxes. Property taxes notices are send around October 1st, but are not due until the end of the year. Texas is a community-property state.

Lenders handle about 60% of the escrows and title companies handle the rest. Conveyance is by warranty deed. Mortgages and deeds of trust with private power of sale are the security instruments. Mortgage foreclosures require judicial proceedings which take about a year; deed-of-trust foreclosures take advantage of private power-of-sale provisions and take about 4 months. Utahans use ALTA owner’s and lender’s policies and endorsements. Buyers and sellers split escrow fees, and sellers pay the title insurance premiums. There are no documentary, transfer, or mortgage taxes. Property taxes are payable November 30th.

Attorneys take care of closings. Conveyance is by warranty or quitclaim deed. Mortgages are the customary security instruments, but large commercial transactions often employ deeds of trust . Mortgage foreclosures require judicial proceedings for strict foreclosure; after sale, there is a redemption period of one year for mortgages dated prior to April 1, 1968, and 6 months for all others. Vermonters use ALTA owner’s and lender’s policies and endorsements. Buyers pay recording fees, title insurance premiums, and transfer taxes. Property tax payment dates vary across the state.

Attorneys and title companies conduct real estate closings. Conveyance is by bargain-and-sale deed. Deeds of trust are the customary security instruments. Foreclosure takes about 2 months. Virginians use ALTA policies and endorsements. Buyers pay the title insurance premiums and the various taxes. Property tax payment dates vary.

WASHINGTON

Title companies, independent escrow companies, lenders, and attorneys may handle escrows. An attorney must prepare real estate documents, but there is a limited practice rule which lets licensed non-attorneys prepare most of the commonly used real estate documents. Conveyance is by warranty deed. Both deeds of trust with private power of sale and mortgages are used as security instruments. Mortgages require judicial foreclosure. Deeds of trust require that a notice of default be sent first and 30 days later, a notice of sale. The notice of sale must be recorded, posted, and mailed at least 90 days before the sale, and the sale cannot take place any earlier than 190 days after the actual default. Sellers generally pay the title insurance premiums and the revenue tax; buyers and sellers split everything else. Property taxes are payable April 30th and October 31st. Washington is a community-property state.

Attorneys conduct escrow closings, although lenders and real estate agents do them occasionally. Conveyance is by warranty deed, bargain-and-sale deed, or grant deed. Deeds of trust are the customary security instruments. Foreclosures are great for lenders; when uncontested, they take only a month. West Virginians use ALTA policies and endorsements. Buyers pay the title insurance premiums and sellers pay the documentary taxes; they divide the other closing costs. Property taxes may be paid in a lump sum after July 6th or in two installments on September 1st and March 1st.

WISCONSIN

Lenders and title companies conduct what are called “table closings” throughout the state, except in the Milwaukee area, where attorneys conduct the closings. Conveyance is by warranty deed, but installment land contracts are used extensively, too. Mortgages are the customary security instruments. Within limits, the actual mortgage wording determines foreclosure requirements; redemption varies from 2 months for abandoned property to a full year in some cases. Lenders generally waive their right to a deficiency judgment in order to reduce the redemption period to 6 months. Wisconsinites use ALTA policies and endorsements. Buyers generally pay closing costs and the lender’s policy fees; sellers pay the owner’s policy fees and the transfer taxes. In transactions involving homesteads, conveyances may be void if not joined into by the spouse. Property taxes may be paid in full on February 28th, or they may be paid half on January 31st and half on July 31st. Wisconsin is a quasi-community-property state.

Real estate agents generally conduct closings. Conveyance is by warranty deed. Mortgages are the usual security instruments. Foreclosures may follow judicial or power-of-sale proceedings. Residential foreclosures take around 120 days; agricultural foreclosures, around 13 months. Wyomingites use ALTA owner’s and lender’s policies and endorsements. Buyer and seller negotiate who’s going to pay the various closing costs and title insurance fees. There are no documentary, mortgage, or transfer taxes. Property taxes may be paid annually December 31st or semi-annually September 1st and March 1st.

All Rights Reserved. Distributed by Escrow Publishing Company. This article may not be resold, reprinted, resyndicated or redistributed without the written permission from the publisher.