When Selling a House, Avoid Awkward Misunderstandings Over Fixtures and Furnishings

State-of-the-art appliances, sleek lighting fixtures and tasteful window treatments can all make a memorable impression on potential home…

State-of-the-art appliances, sleek lighting fixtures and tasteful window treatments can all make a memorable impression on potential home…

Real estate closings can be fraught with complications and setbacks, but they can go smoothly and quickly —…

Kristen and Ben had been looking for the right property to buy for over six months. They finally…

In almost all real estate transactions, there are title issues that must be cleared up in order to…

One of the most important decisions that needs to be made at closing is how you choose to…

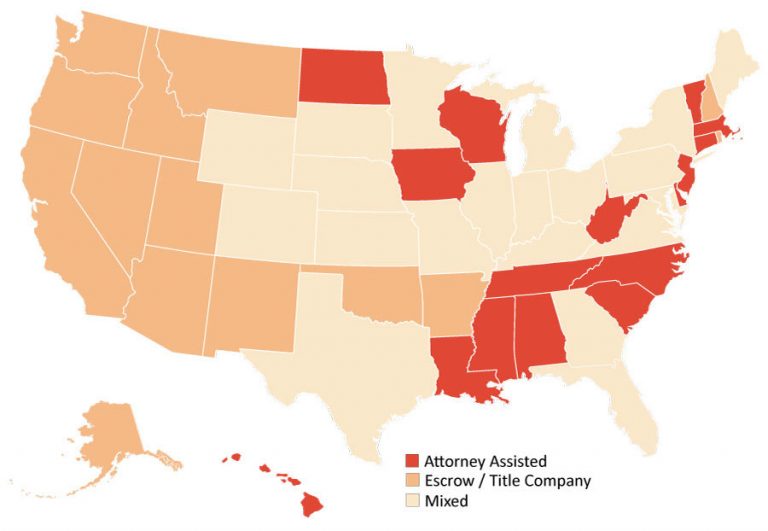

Here is a summary of closing practices for each of the United States. This is a general reference guide. Local practices within your city or county may differ.

Once you have opened escrow and given the escrow officer the details of your purchase, you will next…

As a potential Buyer, you may have have no reason to suspect that an outstanding permit exists on…

Let’s assume that you are in the category of buyers who need to find a property now and…

Most real estate associations have prepared COVID-19 addenda similar to those found in the California addendum, though the…

Title and escrow companies are adapting to the new environment brought on by the COVID-19 virus and taking guidance from the CDC and WHO on how to conduct business to keep their customers and employees safe.

It may be common for you to hear that the builder of the new home you will be…

The Tax Reform Act of 1986 required anyone responsible for closing a real estate transaction, which may include…

Buyer’s Home Closing Checklist Have you made a final walk-thru inspection of the property? Is the condition of…

By Sandy Gadow Special to The Washington Post Ever notice how enticing advertising for newly built houses can…

Real estate closings may be handled by escrow companies, title companies, lawyers, or a combination of one or…

Jack and Eliza searched Fayette county in Virginia for the right house. Not only must it be in…

New York Times April 27, 2012 There’s no lack of information on the Internet about real estate closings….